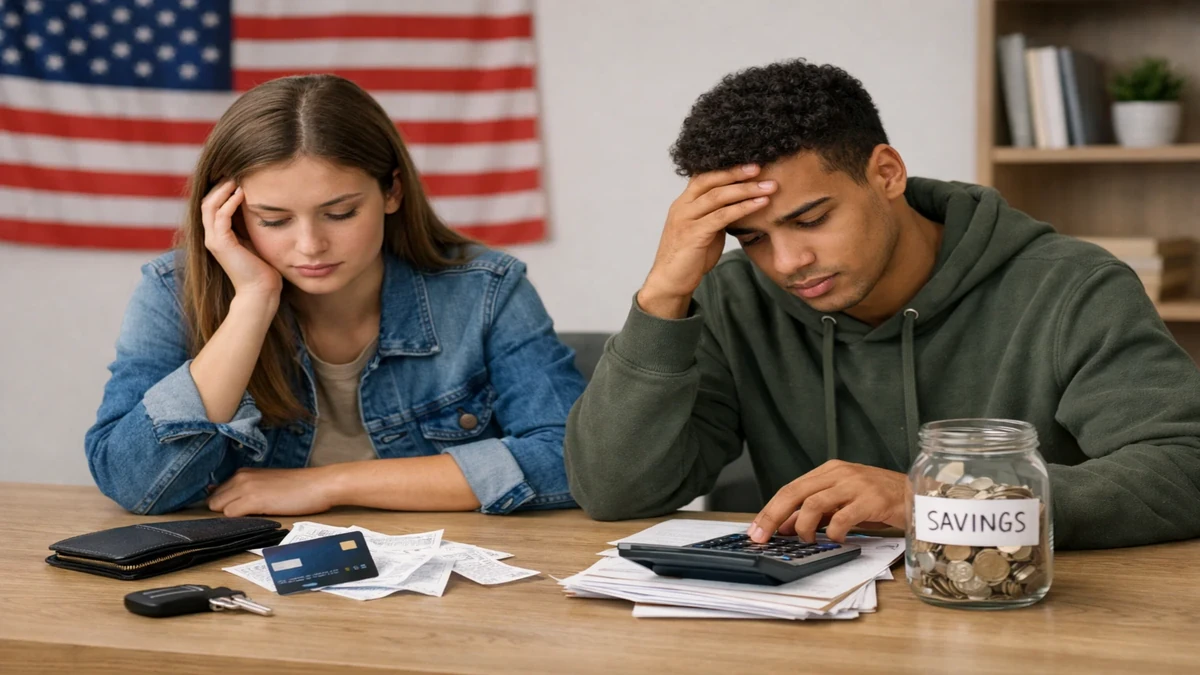

In the United States, the relationship between finances and well-being has become increasingly visible as economic pressure affects daily life. Even households that manage routine expenses with a credit card may experience stress that goes beyond numbers on a balance sheet.

Financial stress as a mental health factor

Financial stress is one of the most common sources of anxiety among U.S. adults. Concerns about debt, income stability and rising living costs can create persistent worry. This stress often accumulates silently, affecting sleep, concentration and overall quality of life. Mental strain does not depend solely on income level, but on perceived control and predictability.

Unclear financial situations intensify this effect. When individuals avoid reviewing accounts or understanding obligations, uncertainty grows. This lack of clarity increases emotional pressure and reduces confidence in decision-making. Improving financial awareness is often the first step toward reducing stress and regaining a sense of control.

Behavioral cycles between money and emotions

Emotions and financial behavior influence each other continuously. Stress can lead to impulsive spending or avoidance of financial tasks, which in turn worsens financial outcomes. This cycle reinforces negative feelings and makes recovery more difficult. Recognizing this pattern is crucial for breaking it.

Positive habits work in the opposite direction. Regular budgeting, savings routines and realistic planning improve confidence and emotional resilience. Small actions create visible progress, which reduces anxiety. Information plays a key role by turning vague concerns into manageable steps.

Building financial well-being alongside mental health

Financial well-being goes beyond having sufficient resources. It includes feeling secure, informed and capable of handling challenges. In the U.S., households that prioritize clarity and planning tend to experience lower stress, even during economic uncertainty. Well-being is shaped by structure, not perfection.

Communication also supports mental health. Discussing finances within families reduces isolation and aligns expectations. Shared understanding prevents silent pressure and unrealistic assumptions. Transparency strengthens both financial and emotional relationships.

Support systems are equally important. Financial education, counseling and digital tools can provide guidance and reassurance. Seeking help should be seen as proactive, not as a sign of failure. Access to reliable information empowers individuals to take constructive action.

Ultimately, the connection between finances and mental health in the U.S. highlights the human side of money management. Numbers alone do not determine well-being; perception and behavior matter just as much. By improving financial clarity and habits, individuals can reduce stress and build stronger Finances that support both economic security and emotional balance.

Read more: Financial automation in the U.S.: limits of fully digital control