Moving through 2026, many households across the United States are rethinking how they manage money as everyday expenses evolve in unpredictable ways. Adapting to these shifts requires more than cutting back; it involves understanding trends, adjusting priorities, and building a flexible financial strategy that fits real life.

Understanding rising expenses in everyday life

Across major cities and smaller communities alike, housing remains one of the most significant financial pressures. Rent and mortgage rates have continued to fluctuate, often outpacing income growth, leaving many individuals searching for creative ways to maintain stability without sacrificing comfort.

Groceries have also become a sensitive point in household spending. Price variations influenced by supply chain adjustments and climate-related factors have made it harder to predict monthly food costs, encouraging people to rethink how and where they shop.

Transportation expenses have followed a similar path, with fuel prices shifting frequently and maintenance costs rising. Many workers now consider hybrid or remote options not only for convenience but also as a practical way to reduce commuting expenses.

Healthcare remains another area where budgeting requires attention. Even with insurance, out-of-pocket costs for medications, consultations, and preventive care can accumulate quickly, pushing families to plan more carefully for unexpected needs.

Utilities, including electricity, water, and internet services, have gradually increased in many regions. These recurring costs may seem small individually, but together they can significantly impact overall financial balance if not monitored consistently.

Adapting spending habits to modern realities

In response to these changes, many households are shifting toward more intentional spending. Rather than focusing solely on cutting costs, people are prioritizing value, choosing purchases that offer long-term benefits instead of short-term satisfaction.

Digital tools have become essential in managing finances more effectively. Budgeting apps and automated tracking systems allow users to visualize their spending patterns clearly, making it easier to identify areas where adjustments can bring meaningful results.

Lifestyle adjustments are also playing a key role in financial resilience. Cooking at home more frequently, exploring local entertainment options, and reducing impulse purchases are practical ways individuals are aligning their habits with current economic conditions.

Another important shift involves redefining what is considered essential. As financial pressures evolve, many people are reassessing their priorities, distinguishing between needs and wants in a more thoughtful and personalized manner.

Social influences, including online trends and peer behavior, continue to shape spending decisions. However, those who maintain a strong sense of financial awareness are better equipped to resist unnecessary expenses and stay aligned with their long-term goals.

Building a resilient monthly plan

Creating a sustainable monthly plan begins with a clear understanding of income sources. Whether earnings come from a single job, freelance work, or multiple streams, knowing exactly how much money enters the household is the foundation of effective planning.

From there, categorizing expenses becomes essential. Fixed costs such as rent, insurance, and subscriptions must be accounted for first, ensuring that essential obligations are consistently covered before allocating funds to more flexible categories.

Savings should no longer be treated as an afterthought. In the current economic landscape, setting aside money regularly, even in small amounts, helps build a financial cushion that can absorb unexpected challenges without disrupting daily life.

Debt management is another critical component of a well-organized plan. Prioritizing high-interest obligations while maintaining minimum payments on others can gradually reduce financial pressure and free up resources for future investments.

Flexibility remains a defining feature of a strong monthly strategy. Rather than adhering to rigid structures, successful planners adjust their approach as circumstances change, allowing them to respond effectively to both opportunities and setbacks.

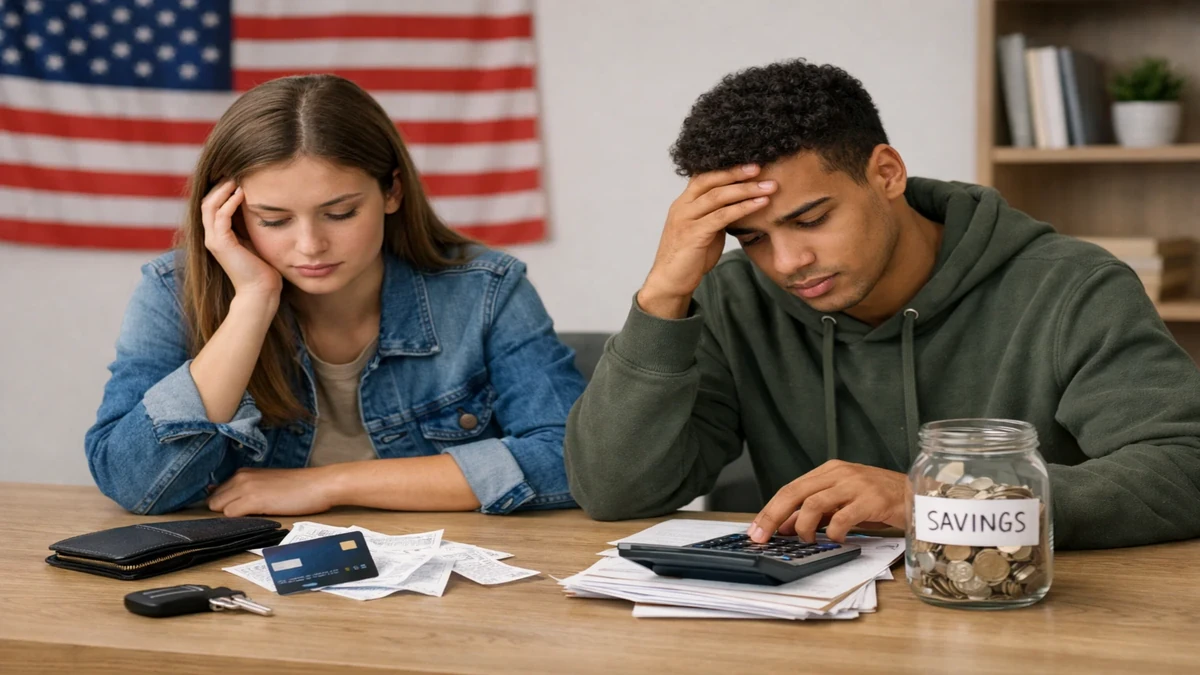

Managing unexpected financial pressure

Unpredictable events can disrupt even the most carefully planned budgets. Job changes, medical emergencies, or sudden repairs often require immediate attention, making it essential to maintain a level of preparedness within financial planning.

Emergency funds serve as a vital safety net in these situations. Having accessible savings dedicated to unforeseen expenses reduces reliance on credit and prevents long-term financial strain caused by high-interest borrowing.

Insurance coverage also plays a protective role, helping mitigate the impact of significant expenses. Reviewing policies regularly ensures that coverage remains adequate and aligned with current needs, avoiding gaps that could lead to costly surprises.

Emotional responses to financial stress can influence decision-making in challenging times. Maintaining a calm and structured approach helps individuals avoid impulsive choices that may worsen their situation rather than improve it.

Seeking guidance, whether from financial advisors or trusted resources, can provide clarity during uncertain moments. External perspectives often reveal solutions that may not be immediately apparent when facing pressure alone.

Planning for long-term stability

Looking beyond immediate needs, long-term stability requires a forward-thinking mindset. Retirement planning, for instance, has become increasingly important as individuals recognize the need to secure their future in an evolving economic environment.

Investments, when approached thoughtfully, can support financial growth over time. Diversifying assets and understanding risk levels allow individuals to build portfolios that align with their goals while adapting to changing market conditions.

Education and skill development also contribute to financial resilience. By enhancing professional capabilities, individuals increase their earning potential, creating more opportunities to navigate rising costs effectively.

Housing decisions, whether renting or buying, should be evaluated carefully with long-term implications in mind. Stability, location, and affordability must be balanced to ensure that choices made today remain sustainable in the future.

Ultimately, achieving financial balance in 2026 involves a combination of awareness, adaptability, and intentional planning. By understanding evolving expenses and reorganizing priorities, individuals can build a budget that not only survives change but thrives within it.